CS134 Project Milestone Report

A Machine

Learning System for Stock Market Forecasting

My email: Jianfeng.Huo@dartmouth.edu

Motivation:

Recently,

a large amount of amazing work has been done in the area of analyzing and

predicting stock prices and index changes using Machine Learning Algorithms.

Intelligent Trading Systems has been used for most of the stock traders to help

them in predicting prices based on various situations and conditions, thereby

helping them in making instantaneous investment decisions. Stock market

prediction is regarded as one of the most challenging task in financial

time-series forecasting. This is primarily because the underlying nature of the

uncertain financial domain and in part because of the mix of known parameters

(Previous Day’s Closing Price, P/E Ratio etc.) and unknown factors (Election

Results, Rumors etc.).

In my project, I will implement a machine learning

system which is proposed by Lijuan Cao and Francis

E.H. Tay [1] based on Support Vector Machines (SVMs)

for stock market prediction. SVMs were originally developed by Vapnik for

pattern recognition problems. In this case we try to find an optimal hyperplane

that separates two classes. In order to find an optimal hyper plane, we need to

minimize the norm of the vector w, which defines the separating hyper

plane. This is equivalent to maximizing the margin between two classes.

Recently with the introduction of ε-insensitive loss function, SVMs has been

extended to solve non-linear repression problems. In the case of regression,

the goal is to construct a hyperplane that lies "close" to as many of

the data points as possible. Therefore, the objective is to choose a hyperplane

with small norm while simultaneously minimizing the sum of the distances from

the data points to the hyperplane. Both in classification and regression, we

obtain a quadratic programming problem where the number of variables is equal to

the number of observations [4].

Method:

Regression

approximation emphasizes the problem of estimating a function based on a given

set of data ![]() (xi is the input vector and di is the desired

value), which is produced from the unknown function. SVMs approximate the

function in the following form:

(xi is the input vector and di is the desired

value), which is produced from the unknown function. SVMs approximate the

function in the following form:

Where

![]() are the features of inputs and

are the features of inputs and ![]() , b are coefficients. Thus they are estimated by minimizing the

regularized risk function (2):

, b are coefficients. Thus they are estimated by minimizing the

regularized risk function (2):

In

equation (2), the first term ![]() is the ε-insensitive loss

function. It is a self-explanatory function that indicates the fact that it

does not penalize errors below ε. The second term

is the ε-insensitive loss

function. It is a self-explanatory function that indicates the fact that it

does not penalize errors below ε. The second term ![]() is used as a measure of

function smoothness. C is a prescribed constant representing determining the

trade-off between the training error and model smoothness. Introduce slack

variables ζ, ζ* to the above equations we have the following

constrained function:

is used as a measure of

function smoothness. C is a prescribed constant representing determining the

trade-off between the training error and model smoothness. Introduce slack

variables ζ, ζ* to the above equations we have the following

constrained function:

Minimize:

Subject to:

![]()

![]()

![]()

Thus, Eq. (1) becomes the following explicit form:

Lagrange Multipliers.

In

function (5), ![]() are the Lagrange multipliers

introduced. They satisfy the

are the Lagrange multipliers

introduced. They satisfy the ![]() equality

equality![]() , and they can be obtained by maximizing the dual form of function

(4), which has the following form:

, and they can be obtained by maximizing the dual form of function

(4), which has the following form:

With the following constraints:

![]()

![]()

This

is a quadratic programming problem and only a number of coefficients ![]() will be assumed to be nonzero

and the data points associated with them can be referred to as support vectors.

will be assumed to be nonzero

and the data points associated with them can be referred to as support vectors.

Experiment:

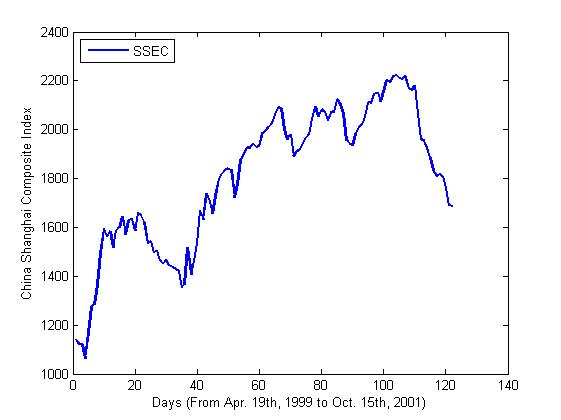

The SSEC Index in Shanghai Mercantile is selected for the

experiment. We choose Every Wednesday’s Close price adjusted for dividends and

splits from Apr. 19th, 1999 to Oct. 15th,

2001 as the input data for the experiment. The main reason for choosing this

period is that it contains an obvious collapse during this period which is

shown in figure 1. We use ε-SVM to train the first 80 data and then predict the

rest of the data. The error of the training and predicting procedure is

measured by Root-Means-Square-Error (![]() )

)

Figure

1- Index of SSEC (Apr. 19th, 1999-Oct. 15th,

2001)

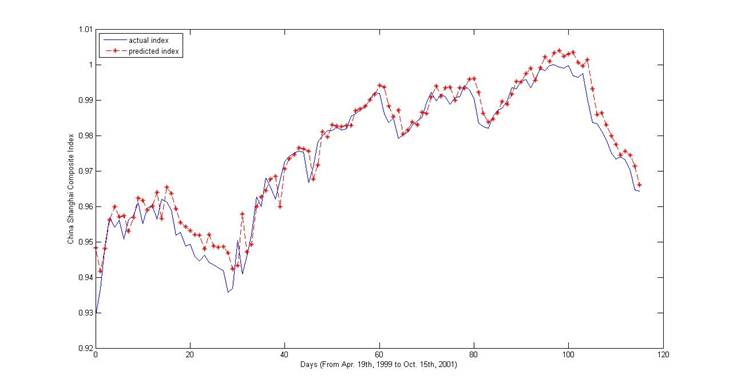

Before predicting we did a simple preprocessing with the original

data. As unusually done in the economic analysis, we did a logarithmic

transformation to the data and then scale it into the range of [0, 1]. We

choose Gaussian Radial function as the kernel function in the experiment. For

each train set, we use the previous six days’ data to predict the seventh day’s

price. There are 74 sets of training data (i.e. 80 days’ market indices) that

is to say we will discover and memorize the sequence’s statistical law through

the previous 80 days’ data and predict the rest days’ indices in the period.

The result is shown in figure 2. The blue line represents the actual index of

the market and the red stars represent the output from the SVM. The training

error is 0.0061 and the testing error is 0.0078.

Figure 2-experiment result

To do:

l • Add more technical indicators as the input features

l • Have a study of the sensitivity of SVMs to parameters

l • Apply the system to more stock markets, e.g. DJI

Timeline:

l Read papers about using SVM for stock market prediction

l Before milestone implement the hybrid machine learning system in Matlab.

l Before final debug the algorithm, test data and improve accuracy of the system.

l Analyze experiment results and write the final report.

Reference

[1] L. J. Cao and F. E. H. Tay, "Financial

forecasting using support vector machines", Neural Comput.

Applicat., vol. 10, no. 2, pp. 184-192, 2001.

[2] Vatsal H. Shah, “Machine Learning Techniques for Stock Prediction”, http://www.vatsals.com/Essays/MachineLearningTechniquesforStockPrediction.pdf

[3] R. Choudhry and K. Garg, "A hybrid machine learning system for stock

market forecasting," Proceedings of World Academy of Science, Engineering

and Technology, vol.29, pp. 315-318, 2008.

[4]T. B. Trafalis and H. Ince. Support

vector machine for regression and applications to financial forecasting.

IJCNN2000, 348-353

[5] http://in.finance.yahoo.com/